.png)

A recent report by the Brookings Institution has stirred up the debate about whether there is a looming student loan crisis. But there is no question that with a growing number of people in college and rising tuition costs, more and more students are taking on loans and face years of paying down that debt— whether they successfully graduate or not.

To illustrate a simple measure of the growing debt from student loans, Chmura built the maps below from Federal Reserve Bank of New York (“FRBNY”) Consumer Credit Panel data to show the balance of student loan debt per capita in each state between 1999 and 2012.

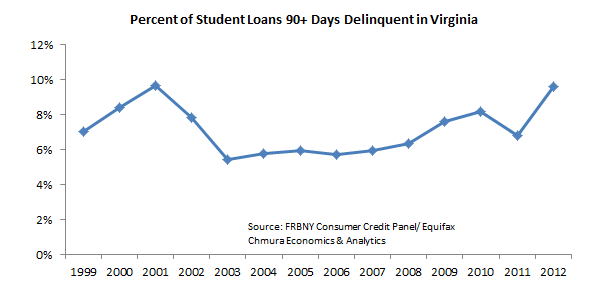

To use Virginia as an example, student loans stood at $580 per capita in 1999; by 2012 that had increased 597% to $4,040 (note that the data are not adjusted for inflation). The average student loan per borrower in Virginia was $26,310 in 2012, compared with an average of $24,810 across the United States. As for fears about graduates not being able to pay off their debt, the percentage of student loan debt balance 90+ days delinquent in Virginia rose 2.79 percentage points between 2011 and 2012, but was still comparable to historic levels. It is important to note in interpreting this data, though, that the percentage of delinquent loans may be similar to that of a decade ago, but with increasing enrollments a lot more people in the state are having difficulty paying off their student loans. In addition, many loans have six-month grace periods before requiring payments, and there are a variety of options to postpone or decrease payments that graduates who are unemployed or low-income can use to prevent default.

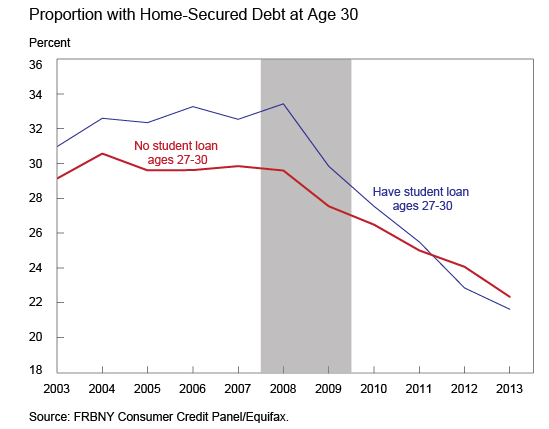

So is this additional debt impacting any other financial decisions, especially among young households? Analysis released by the FRBNY using the same data series suggests a shift in homeownership among student borrowers age 30 and younger:

However, the recession brought a sudden reversal in this relationship. As house prices fell, homeownership rates declined for all types of borrowers, and declined most for those thirty-year-olds with histories of student loan debt. In last year’s blog, we reported that 2012 was the first time in at least ten years that thirty-year-olds with no history of student loans were actually more likely to have home-secured debt than those with a history of student loans… student loan holders were still less likely to invest in houses than nonholders in 2013, despite the marked improvements in the aggregate housing market.” (Emphasis added)

The data from FRBNY and Brookings Institute suggest that a crisis of young borrowers unable to pay off their student loans may not be a concern in the near future, but with over 40% of young adults (25 years old) carrying student debt, the rise in student debt over the past decade is likely preventing those households from contributing to a recovery in the housing market today.